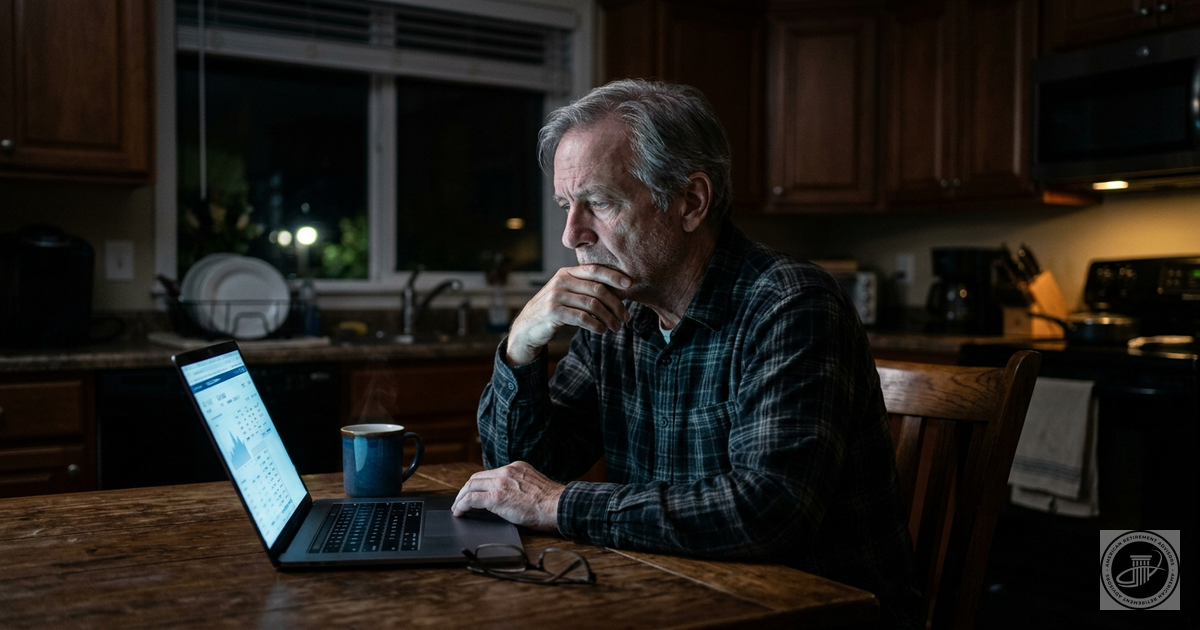

It is 2 AM and you are wide awake.

You rolled over 20 minutes ago. Then you rolled back. Now you are staring at the ceiling, doing math you have already done a hundred times. The market dropped again today. Or maybe it did not drop, but someone on the news said it might. Your brother-in-law mentioned something about Bitcoin at dinner. You do not own Bitcoin. You are still thinking about it at 2 AM.

You get up. You open your laptop at the kitchen table. You log into the brokerage account and look at the number. It is the same number it was yesterday. You do not feel better. You check a CD rate. You Google "best savings rate right now." You read half an article about the Fed. You close the laptop. You go back to bed. You do not sleep.

Your spouse asks you in the morning if everything is okay. You say yes. Everything is fine. The house is paid off. The kids are grown. You have more money sitting in accounts than you have ever had in your life. Everything is fine.

But it does not feel fine. And you cannot explain why.

The Worry Loop

That 2 AM routine is more common than you think. We see it every week when someone finally walks through our door. They sit down, shoulders tight, and start pulling out statements. They do not have one clean question. They have a dozen scattered ones that all come from the same place. "What happens if the market crashes again?" "Should I be doing something different with this IRA?" "My neighbor moved everything into CDs, should I do that?" "What if one of us needs long-term care?"

They have been carrying those questions around for months. Sometimes years. Checking accounts, reading headlines, comparing rates, running numbers on napkins. Not because something is wrong. Because they cannot prove to themselves that everything is right.

One of our advisors, Kyle Jacobs, puts it this way: "Thinking you have enough money, knowing you have enough money, are two very different items." That gap between thinking and knowing is where the 2 AM math lives. That is where the worry loop runs.

What Breaks the Loop

The worry does not stop because someone tells you to stop worrying. It stops when someone shows you.

That is what actually happens when people sit down with our team. We do not give a pep talk. We open a screen and walk through the numbers together. Here is your income. Here is what you spend. Here is what happens if the market drops 30% tomorrow. Here is what happens if you live to 95. Here is what happens if your spouse needs long-term care. And here is what your life looks like on the other side of all of it.

My father has been doing this for over 25 years. He has shown it to hundreds of people. It lands the same way every time. Not because he is telling them they are okay. Because they can see it. The numbers are on the screen. The scenario is modeled. The worst case is right there, and it is not as bad as what they were imagining at 2 AM.

One client told our advisor Marc Frye, after seeing her plan laid out for the first time: "I appreciate you so much. Thank you, thank you, I can sleep now." Another told our team: "I have an anxiety level, and it's gotten a lot better since I've started talking to both of you."

That is what a plan does. It does not change the numbers. The numbers were fine before they walked in. It changes the feeling. Because now they can see it. And once you see it, the 2 AM math stops.

For the first time in years, people start talking about what they actually want to do. Not what they are afraid of. What they want.

The Question That Changes Everything

There is a question that almost never comes up in a first meeting: "What do I want my retirement to look like?"

People come in with a folder of statements. They have their Social Security estimates. They have questions about Roth conversions and RMDs and Medicare premiums. They have done their homework on the money part.

But ask them what they want to do with their time, what makes them feel alive, what they would do tomorrow if money were not a factor, and most people go quiet. The whole system trained them to save, save, save. The part that comes after? That is on you to figure out.

That is the real planning gap. Not the money. The meaning.

What I Have Watched People Discover

I work with retirees every day. And the ones who are the happiest are not the ones with the biggest accounts. They are the ones who figured out what the money is for.

One couple started volunteering at a food bank three mornings a week. They told me it was the first time since retiring that they felt like they had a schedule worth keeping.

Another client picked up woodworking. Spends every afternoon in his garage building furniture for his grandkids. He told our advisor, "I used to check my portfolio every morning. Now I check my lumber supply."

A woman who retired from teaching started tutoring neighborhood kids for free. She said she missed feeling useful. Not busy. Useful.

And then there was the woman in one of our meetings who said, plainly: "I have cancer right now. And I'm trying to make my husband promise that when I get to the other side of this, that we go to Tahiti for 10 or 14 days." She was not asking about her portfolio. She was asking about her life. That is what money is for.

None of those things cost much money. All of them changed everything.

The Risk That Actually Shows Up

Everyone worries about running out of money. That is the headline fear. But the risk that actually shows up more often is running out of purpose.

I have seen people with more than enough savings who are miserable. Not because of their portfolio. Because they wake up every day with nowhere to be and nothing that needs them. They traded a career that gave them structure for a retirement that gave them a couch and a remote control.

And then they fill the void with worry. Market worry. Health worry. Rate worry. Bitcoin worry. It is not really about any of those things. It is about needing something to care about.

The money was never the point. The money was the tool. And if you forget what the tool is for, you just end up polishing it forever.

Kyle Jacobs tells our clients: "It's not the last chapter. It may be the last volume in the series, but there are plenty of chapters to be written during this time." He is right. But you have to pick up the pen.

A Different Kind of Checklist

If you have been retired for a while and something about this hits home, try this. Forget the portfolio for one week. Instead, answer three questions:

1. What made me feel proud this month?

2. When was the last time I lost track of time doing something I enjoyed?

3. If I found out I had exactly enough money to last the rest of my life, no more and no less, what would I do differently starting tomorrow?

That third one is the one that matters. Because for most people, the answer is: nothing about the money would change. What would change is the worry. And if the worry is the only thing standing between you and the life you actually want, then the worry is the problem. Not the money.

You Already Did the Hard Part

You raised kids. You showed up for 30 years. You saved when it was hard. You made sacrifices nobody saw. You got here.

And "here" is exactly where you were trying to get to all along.

My father tells clients this all the time: "You've earned your way past that requirement, so you can quite honestly do whatever you want, whenever you want." He means it. And he is usually right.

So maybe today is the day you look around instead of looking up. Maybe today is the day you stop checking the score and start playing the game you spent your whole life earning the right to play.

You already won. You just forgot.

And if you need someone to show you the math that proves it, that is what we are here for. Not to sell you something. Not to move your money around. Just to show you, clearly and simply, that you are going to be okay. So you can get on with the business of actually living.